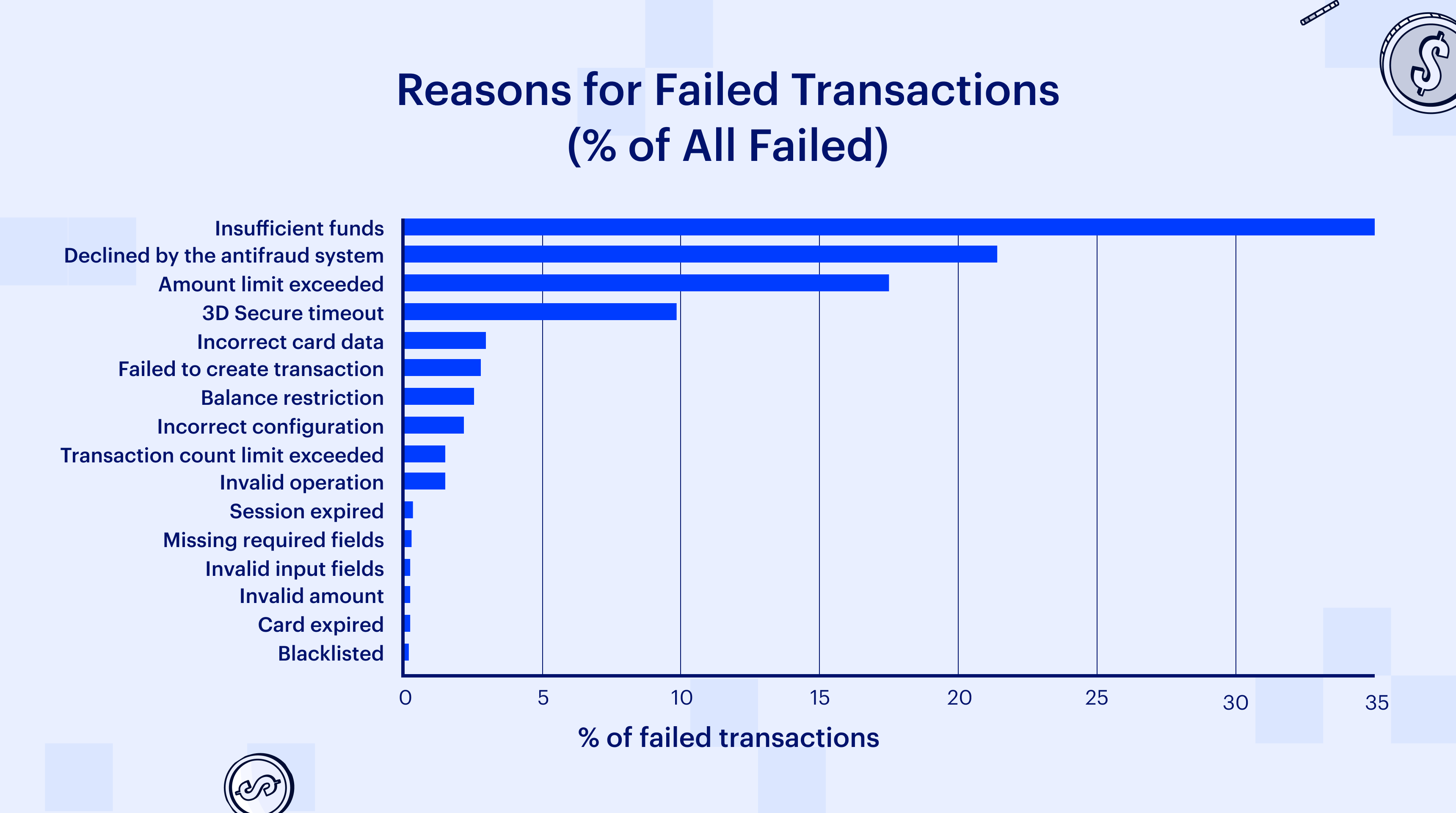

The effectiveness of a payment infrastructure is determined not only by the number of successful transactions but also by the depth of understanding of the reasons for failures. A high decline rate is not always a technical problem – in many cases, it signals strategic gaps in the design of the payment process, the settings of anti-fraud systems, or communication with issuing banks.

To fully grasp what is a payment orchestration, it’s important to understand that it’s more than just transaction routing — it’s a comprehensive approach to coordinating all elements of the payment stack, from gateways and acquirers to fraud tools and payment methods. Tranzzo applies this principle at scale to maximize acceptance and efficiency.

The Tranzzo team's analytics are based on processing millions of transactions every month with a wide geographic and industry coverage. This allows us not only to identify common causes of failed payments but also to design solutions that systematically reduce decline and chargeback rates while maintaining the security of the payment environment.

⬇️ Further in the article, you will get acquainted with our exclusive decline classification, quantification, and business impact assessment analytics. We will also look at practical mechanics that ensure a steady increase in acceptance rates.

Most Popular Payment Methods in the World: Analysis by Markets

Most Popular Payment Methods in the World: Analysis by Markets How to Increase Conversions in an Online Store with a Checkout Page

How to Increase Conversions in an Online Store with a Checkout Page How Tranzzo Simplified the Payment Process for Tickets.ua

How Tranzzo Simplified the Payment Process for Tickets.ua Integrating Multiple Payment Methods: Challenges and Solutions

Integrating Multiple Payment Methods: Challenges and Solutions Abandoned Shopping Carts: Why Businesses Lose Revenue and How to Increase the Number of Successful Payments

Abandoned Shopping Carts: Why Businesses Lose Revenue and How to Increase the Number of Successful Payments